News

Speer: Dairy Cows Now On Double Duty

The dairy industry’s productivity gains during the past several decades are truly remarkable. It’s not really a story that gets told very often; popular media regularly touts declining milk consumption in the United States. However, that does NOT mean dairy demand is waning. To the contrary, it’s robust and America’s dairy producers have done an incredible job of meeting that demand (along with facilitating growth in exports, too).

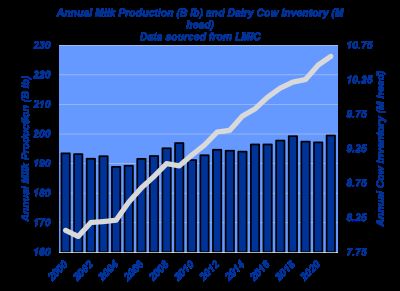

That’s occurred because of steady gains in milk production year after year – going from roughly 165B lb annually to nearly 230B lb during the past twenty years. But most significant, that’s all happened while dairy cow inventory has remained relatively unchanged. (see first graph)

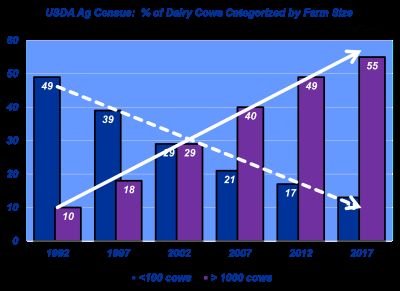

However, those gains have also meant ongoing consolidation within the dairy sector. Business analyst Michael Hammer’s timeless observation portrays it best: “Increasing productivity does enable a company to lower its costs while increasing its output and that ought to be good for any business. But what is good for any business, it turns out, isn’t good for every business.” Twenty-five years ago nearly half of all dairy cows were maintained by dairies with less than 100 cows. Now jump to the latest census (2017): 55% of cows are maintained by dairies with 1000-or-more cows. (see second graph)

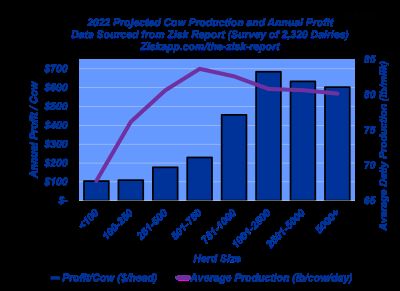

Commodity businesses are inherently challenging – average returns hover around breakeven. Staying in front of that reality generally requires getting bigger; economies of scale provide significant cost advantages to larger producers. For example, Zisk survey data indicate that production differences are negligible beyond 500 cows; however, getting bigger does facilitate cost savings and subsequent profitability: “…the nationwide move towards larger herd size is born out in terms of profitability.” (see third graph)

That background brings us back to the subject of BeefX. For example, a 1500-cow dairy now has potential to produce 950 head of beef-cross steer calves annually - distributed fairly evenly across a 12-month period. Assuming several of those dairies together in close proximity, suddenly it’s possible to pick up 50-to-100 head of beef-sired, like kind calves (genetics, age) every single week – and subsequently manage them for a specified program. Then consider the Zisk survey – it includes data from 62 dairies with 5000-or-more cows (the average being 11,644 cows)!

It’s also important to account for the business orientation among larger dairies. It’s probably best described by some summary observations in Purdue University’s Large Producer Survey (2021): “The [large] producer of tomorrow is aggressively seeking growth opportunities utilizing a business strategy that is tailored to their unique skills and situation.”

Accordingly, there’ll be increased interest from dairies for retained ownership and/or contractual opportunities that facilitate additional revenue to the operation. And that business orientation works both ways. Given the opportunity for large numbers of consistent, value-added, easily traceable cattle means it won’t just be supply push from the dairy, there’ll also be demand pull downstream. As noted in my previous column, “The beef industry now has a new source of production (BeefX steers) from what used to be considered a highly discounted after-thought (straight dairy steers/ heifers).”

Historically, we’ve often thought of the beef and dairy industries as being separate (with minimal crossover and/or interests). But that’s changing; BeefX potentially will become an integral, sought-after constituent of U.S. beef supply. Dairy cows are now on double duty.

Nevil Speer is an independent consultant based in Bowling Green, KY. The views and opinions expressed herein do not reflect, nor are associated with in any manner, any client or business relationship. He can be reached at nevil.speer@turkeytrack.biz.

CATEGORIES

LATEST NEWS

CONTACT US

Mobile:+86-18612182039

Tel:+86-029-85274126

Whatsapp:+8618612182039

Email:info@watarbio.com

Add:No. 12, Hongzhuan South Road, Yanta District, Xi’an 710061, China